The Appraisal World Just Changed: Here’s What You Need to Know

If you’ve been appraising for more than a few years, you know the routine: Open your software, pick a form 1004 for a detached single-family, 1073 for a condo, or 2055 for an exterior-only; fill it out; attach your addenda; and deliver. Rinse, repeat.

That routine is over.

As of September 2025, Fannie Mae and Freddie Mac officially launched the Limited Production Period for UAD 3.6 and the redesigned Uniform Residential Appraisal Report (URAR). By November 2, 2026, every new appraisal delivered to the GSEs must use the new standard. UAD 2.6, the format that has governed appraisal reporting since roughly 2011, will be retired by May 2027.

This isn’t a tweak. It’s a complete rebuild of how appraisal data is captured, structured, and delivered. Read More at GosourceVal

So, What Actually Changed?

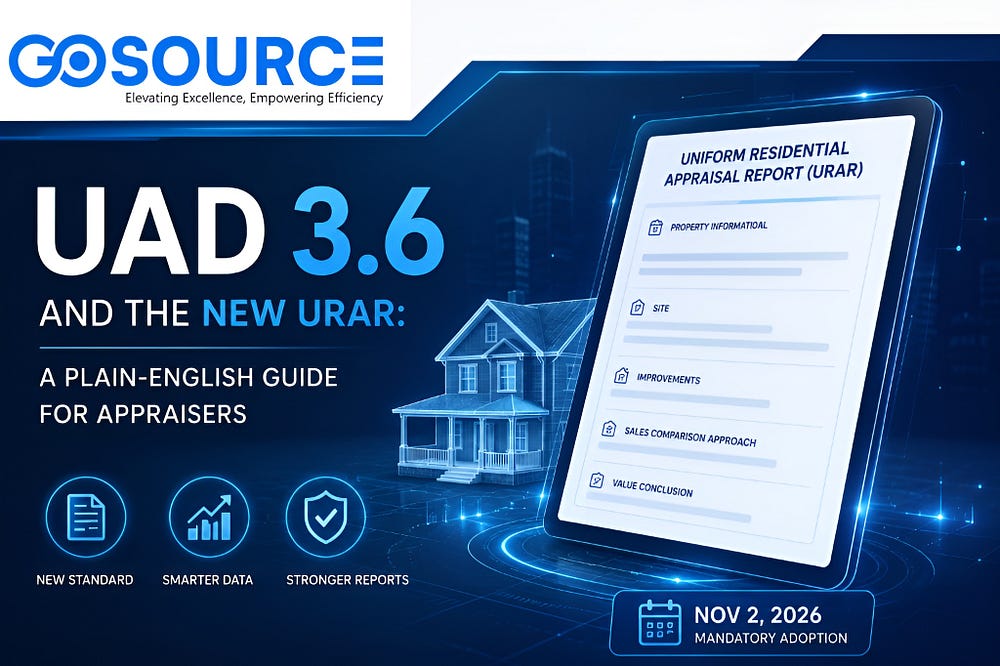

The biggest visible change is the elimination of multiple static forms in favor of a single, dynamic URAR. That one report handles single-family, condos, 2–4 units, manufactured housing, co-ops, hybrids, desktops, and exterior-only assignments all by toggling sections on or off based on the assignment-specific characteristics.

No more shoehorning a property into the wrong form because nothing fits perfectly. No more separate forms for every scenario.

But the form change is really just the surface. The deeper shift is about data structure.

Under UAD 2.6, large portions of an appraisal lived in free-text narrative boxes, the kind that gave appraisers flexibility but also gave reviewers, lenders, and automated systems a lot of ambiguity to deal with. UAD 3.6 aggressively replaces that narrative freedom with structured, standardized data fields. Conditions of ratings, quality ratings, GLA measurements, ADU details, and property characteristics are now captured as discrete, machine-readable data points rather than paragraph descriptions.

Why the GSEs Pushed for This

Fannie Mae and Freddie Mac have been building toward data-first collateral analysis for years. Automated collateral tools, appraisal waivers, desktop appraisals, and hybrid appraisals all of these require reliable, consistent, and analyzable data. UAD 3.6 is the infrastructure that makes all that work at scale.

When appraisal data is structured, lenders can run automated QC in seconds. Risk models can compare properties across markets without interpreting narrative text. AI review tools can flag inconsistencies between data fields and photos instantly. The entire downstream mortgage ecosystem, from underwriting to secondary market securitization, becomes faster and more reliable.

This is why industry experts have described UAD 3.6 not as a routine compliance update but as the future of appraisal reporting, a structural modernization of how the mortgage industry values and transmits collateral data.

What This Means for You as an Appraiser

The honest answer: there’s a learning curve, and it’s real.

You’ll work with new terminology. You’ll encounter more granular data fields in categories you’re used to describing in narrative. You’ll need to think more carefully about how you document property characteristics because the structure of the report will enforce consistency in ways the old form didn’t.

The good news is that once the new system is familiar, it should actually reduce friction. Fewer revision requests from reviewers who can’t parse your addenda. More consistent expectations across different lenders and AMCs. Less back-and-forth over ambiguous descriptions.

Your software vendor is your first call. Make sure they’ve completed GSE verification and that your workflow is ready before the November 2026 mandate arrives. Both Fannie Mae and Freddie Mac have published sample URARs, inspection and reporting tip sheets, and policy supplements that are worth working through before you take your first UAD 3.6 order.

The Timeline immediately

- September 8, 2025: Limited Production Period began; select lenders can submit UAD 3.6.

- January 26, 2026: Broad Production, all lenders may submit UAD 3.6.

- November 2, 2026: All new GSE appraisals must use UAD3.6

- May 2027: UAD 2.6 fully retired

The window between now and November 2026 is not a waiting period. It’s a preparation period. Appraisers who treat it as a waiting period will be scrambling. Those who start building familiarity now will transition cleanly.

Start Now, Not Later

The best thing you can do today is get your hands on a sample URAR from the Fannie Mae or Freddie Mac UAD resource pages and walk through its section-by-section. Take the GSE-endorsed continuing education; both agencies partnered with major CE providers on a seven-hour course specifically designed for this transition.

The form may look different, and the fields may be new, but the fundamental skill of forming a credible, well-supported opinion of value hasn’t changed. UAD 3.6 just asks you to express that opinion in a more structured, digital-first format.

That’s a reasonable ask for a profession that’s been using essentially the same form since the 1980s. Contact us at GosourceVal.